[Deepdive] How Europe can secure Critical Raw Materials for the Energy Transition

The global transition toward a decarbonized economy marks a fundamental shift in the industrial paradigm: moving from an energy system based on hydrocarbons to one built on a sophisticated architecture of minerals and metals. Central to this transformation is the large-scale deployment of renewable energy infrastructure and the full electrification of the transport sector. This systemic overhaul is underpinned by the availability of Critical Raw Materials (CRMs), elements whose unique physical and electrochemical properties make them indispensable for the energy transition.

Today, the geographic concentration of these supplies exposes Europe to significant vulnerabilities. For instance, China provides 100% of the heavy rare earths used by the EU, Turkey 98% of boron, and South Africa 71% of platinum [1]. Recognizing these risks, both the European Union and the International Energy Agency (IEA) have highlighted a subset of 17 strategic materials as “make-or-break” components, evolving from simple commodities into cornerstones of industrial sovereignty. Let’s introduce some of them.

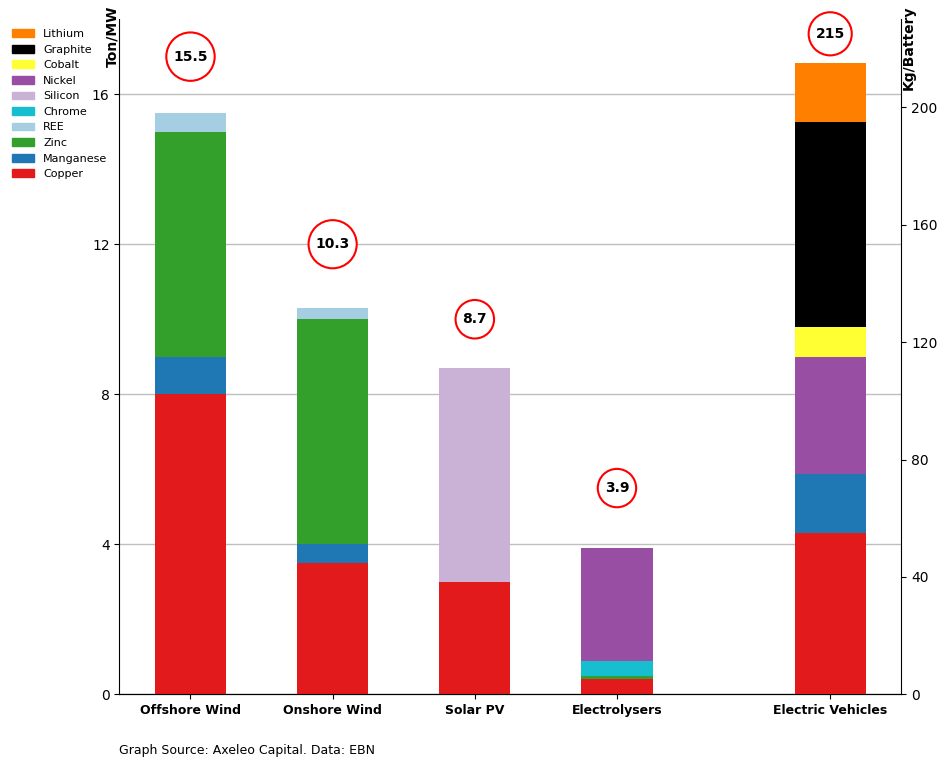

Decarbonizing the economy heavily relies on critical materials such as lithium, cobalt, nickel, graphite, copper, and rare earth elements.

The expansion of the electric vehicle market, and more recently BESS (Battery Energy Storage System), depends on lithium-based battery chemistries, where lithium enables high energy density, cobalt ensures thermal stability and longevity, nickel enhances performance, and graphite supports long-term cycling. Beyond batteries, the broader energy transition requires a massive build-out of grids and generation capacity, with copper serving as the backbone due to its unmatched electrical conductivity. Simultaneously, the conversion of energy into mechanical motion, or the generation of power from wind, relies on the unique magnetic properties of rare earth elements, particularly neodymium and praseodymium, which are essential for high-efficiency permanent magnets used in EV motors and wind turbines.

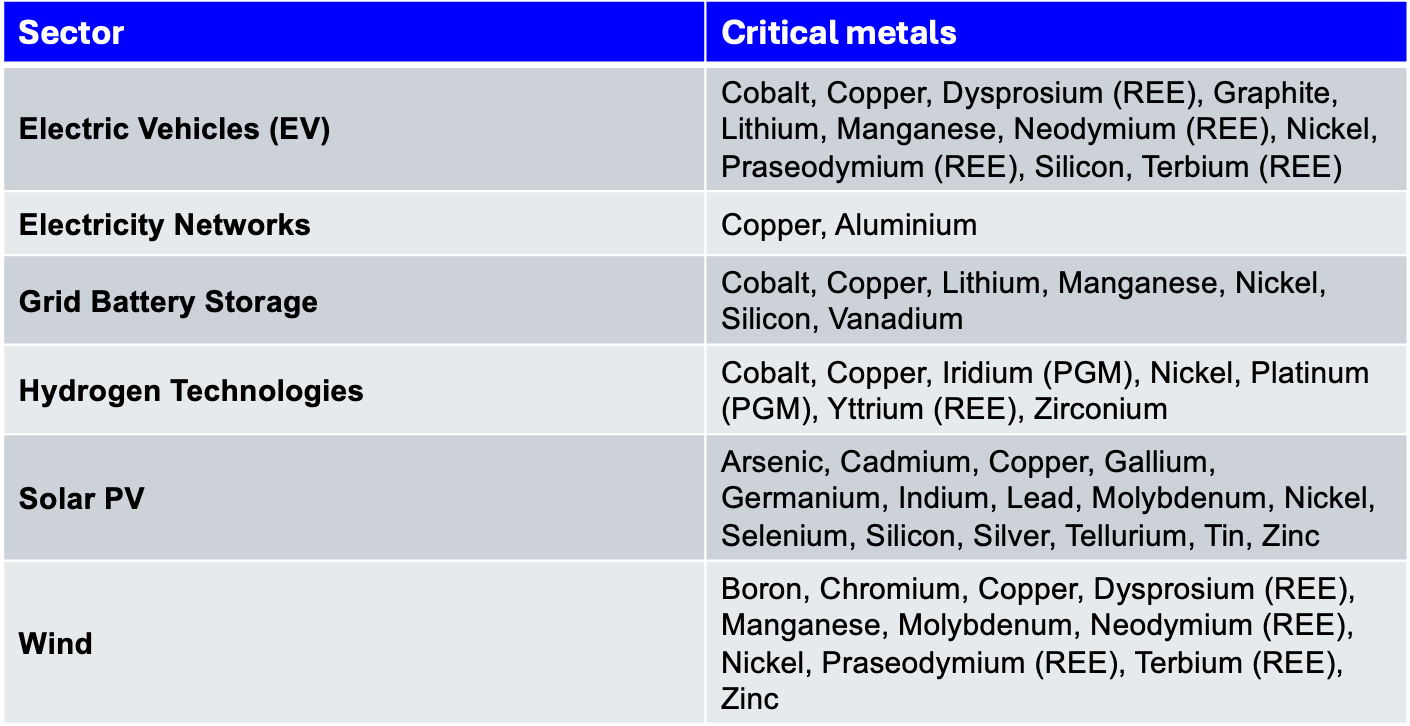

Here is an overview of the critical raw materials required across most modern technologies and industrial systems:

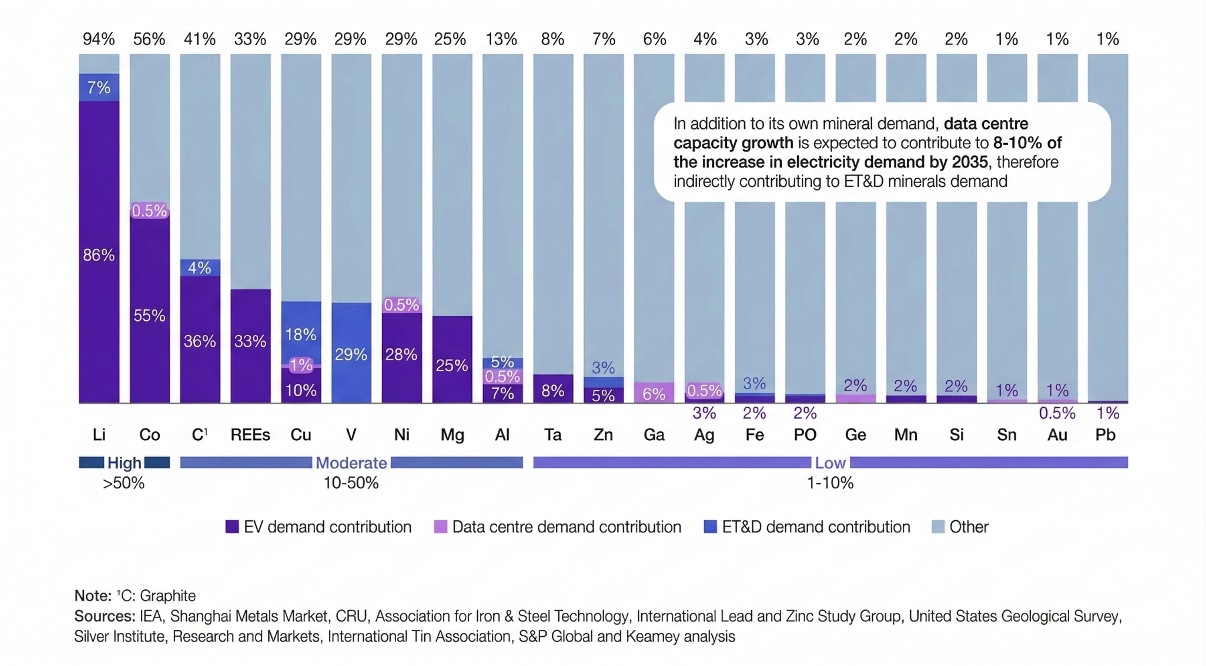

The market tends to focus heavily on battery metals (lithium, cobalt, graphite, nickel) and rare earth magnets (REEs). The IEA and industry experts project that the strongest demand growth will be driven primarily by electric vehicles, as illustrated by estimates of value-chain demand contributions across tracked minerals (share of total global demand in 2035).

According to Benchmark Mineral Intelligence [2], meeting global battery demand by 2030 would require 293 new mines or processing plants. An analysis of major mining projects commissioned between 2010 and 2019 by the IEA shows that it takes on average more than 16 years to bring a project from discovery to first production. In this context, improvements in recycling and processing efficiency are not merely desirable but key for the transition.

Yet, this strong focus on EV-related materials tends to overshadow other essential inputs of the energy transition. Copper, for instance, is a cornerstone of electrification but remains relatively underrepresented, with only a limited number of startups actively working on it today. This narrow prioritization reinforces significant strategic vulnerabilities. For example, despite its critical role in defense and aerospace infrastructure, bauxite (aluminum) is represented in only one of 37 currently identified EU CRM strategic projects [3].

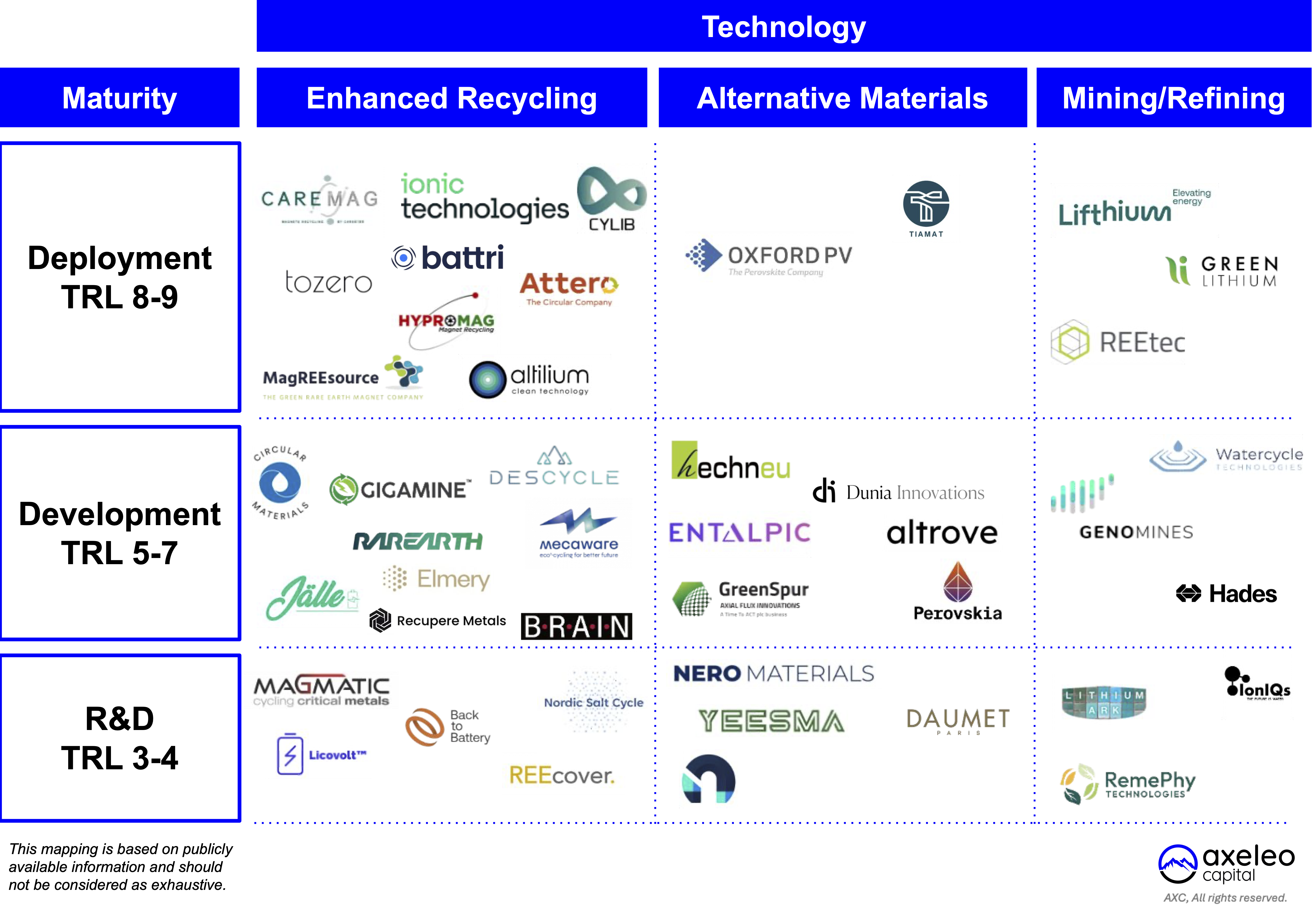

Based on what we have observed, innovation entering the market can be broadly categorized into three waves: enhanced recycling, alternative materials, and modernized mining and refining. Below is a non-exhaustive mapping of the European landscape :

1. Recycling: Mining the Urban Jungle

Recycling is not merely a feel-good narrative; it is a strategic imperative. The EU’s Critical Raw Materials Act (CRMA) sets a clear ambition: by 2030, at least 25% of the EU’s annual Critical Raw Materials consumption must be sourced from recycling. To operationalize this shift and provide regulatory certainty, the EU has paved the way with concrete milestones in the battery sector:

This creates a regulatory tailwind and sends a strong market signal to the battery ecosystem. That said, quantitative regulatory pushes for other critical raw materials are still poorly defined.

We have identified five main trends for waste recycling:

- Batteries: Feedstock supply is maturing. Today, most of blackmass is shipped to Asia [4]. However, next-generation hydrometallurgical technologies could reduce treatment costs enough to compete with the all-in cost of recycling in China plus shipping and regulatory incentives. The key question remains: does Europe have the downstream value chain to process outputs locally, or will they still need to be exported?

- WEEE (Waste Electrical and Electronic Equipment): Only about 40% of waste is collected [5]. Profitability is limited due to high sorting barriers.

- Magnets: Supply is highly fragmented. Recycling wind turbines is profitable, while other sources like WEEE are more abundant but costlier to process. The same question as for batteries applies regarding the utilization of the recycled output.

- Industrial waters: Few players are active in this market, but it represents a growing opportunity. Recycling industrial wastewater means treating and reusing water streams from manufacturing processes. The market is driven by environmental reglementations if the company can’t achieve profitability simply by selling recycled resources.

- Copper: Majority sent to China for input into smelting [6]. 97% of smelting activity concentrated in China, which currently faces negative margin pressures.

The recycling landscape is evolving rapidly, moving from rudimentary processes to sophisticated, science-based solutions. While traditional methods like pyrometallurgy (high-temperature melting) and basic hydrometallurgy (acid-based dissolution) exist, the next generation of deep tech companies are tackling their key limitations: high energy consumption, toxic byproducts, and low recovery rates for certain materials.

Here's where the next wave of disruptive technologies comes in (mapping is not exhaustive):

.png)

Advanced hydrometallurgy is gaining momentum as startups move away from “brute force” acid-based processes toward highly selective, low-toxicity solvents. These solutions act as chemical “keys,” targeting specific metals such as lithium or cobalt with greater precision, improving purity while significantly reducing waste streams. Innovation in this field primarily focuses on two stages of the process.

- The first is leaching, where valuable metals are dissolved into solution. Beyond conventional chemical reagents, some approaches rely on engineered microorganisms, such as bacteria, fungi, or archaea, to extract metals from ores or secondary materials. This bioleaching approach is attracting industrial interest due to its low capital intensity, reduced energy requirements, and modular deployment. However, it remains relatively slow and technologically immature. In Europe, early pioneers include Brain and Magmatic.

- The second stage, purification and recovery, represents a major lever for improvement. Many existing processes rely on sulfate-based chemistries that generate significant pollution. New generations of solvents and resins are now enabling higher recovery rates, lower residual waste, and reduced energy consumption. If these advances deliver on their cost-reduction promises, local recycling could become more competitive than exporting black mass to Asia.

In parallel, molten salt technologies offer a fundamentally different approach. By bypassing several steps of conventional hydrometallurgical processes, molten salts enable direct metal extraction in a single high-temperature phase. This simplification opens the door to smaller-scale, lower-cost facilities with greater operational flexibility. European players such as Descycle (UK) and Nordic Salt Cycle are at the forefront of this emerging segment.

Another highly compelling pathway is direct recycling, which seeks to preserve the functional structure of lithium-ion battery components, particularly cathodes, rather than breaking them down into raw metals. Through thermal or hydrothermal re-lithiation, materials such as NMC cathodes can recover 80–90% of their original capacity, avoiding costly and energy-intensive resynthesis steps. While still nascent in Europe, CellMine (UK) is an emerging player, while Princeton NuEnergy stands out in the United States.

Beyond these core technologies, a broader ecosystem of innovations is taking shape. Companies such as Recupere Metal are advancing copper recycling, while others, including Circular Materials and Weefiner, are developing enabling technologies around water treatment and process efficiency.

The Investment Angle: The largest investments to date have gone to companies focused on EV battery recycling, with players like Redwood Materials and Ascend Elements securing billion-dollar valuations. However, the opportunity is expanding. Look for startups with defensible IP in selective extraction, closed-loop processes, relevant business models, and technologies that can handle the complex, low-volume waste streams of consumer electronics.

2. Alternative Materials & AI Discovery: A Bet on Substitution and Optimization

What if the best recycling starts with no use at all? This is the thesis behind material substitution and optimization. The demand curve for some CRMs may eventually be flattened by new chemistries and materials.

Substitution involves creating alternative materials with equivalent or superior properties. These breakthroughs face a scaling challenge: new chemistries, such as perovskite for solar panel or sodium-ion for battery, must prove they can compete with the economies of scale already achieved by existing gigafactories.

For instance, battery prices have historically fallen by about 13% per year since 1991, but experts [7] consider it physically impossible for costs to continue declining at this pace through 2033. For new chemistries, a critical question is whether they can exceed 300 Wh/kg at $50/kWh, a benchmark comparable to current Chinese Li-ion technology. In addition, Chinese players invest also in these new technologies, scaling them faster.

Similar questions should be asked of any new material seeking to challenge incumbent solutions.

Optimization encompasses innovations such as new alloys, composites, or advanced surface treatments that enhance resistance, conductivity, or magnetic properties. This also covers rare-earth-free motor technologies, which can significantly reduce dependence on critical materials. Such alternatives are especially attractive in the automotive sector, where slightly lower performance can remain acceptable while ensuring functionality and safety. However, they are more challenging in consumer electronics, where miniaturization is key, and in the energy sector, where weight, mechanical constraints, and durability impose stricter performance requirements.

The Investment Angle: If the technology competes with highly mature, capital-intensive sectors like Li-ion batteries or solar panels, the risk is high; Europe currently lacks the industrial capacity and speed to scale as quickly as China. Conversely, targeting less crowded markets, such as catalysts or specialized components that can tolerate slightly lower performance, may present a more attractive opportunity by addressing an existing and favorable market in Europe, unlike hydrogen for instance, which is still largely dependent on energy cost dynamics.

3. Smart Refining & Bio-Extraction: Modernizing the Source

Even with aggressive recycling and substitution, we'll still need to extract a significant amount of new materials. The investment opportunity here is in modernizing a highly centralized and often polluting industry.

- Onshore Refining: More than 80% of global refining capacity is in Asia, primarily China. This creates a geopolitical risk. Startups are tackling this head-on by developing cleaner, more efficient refining processes that can be deployed locally in Europe and North America.

- Bio-Extraction: Similar to bioleaching in recycling, these methods can be applied to mining. Startups like Genomines, who has recently completed a significant round, are using hyperaccumulating plants to literally absorb metals from low-grade ore or mining waste. These plants can then be harvested, providing a clean and low-impact way to "farm" metals.

- Direct Lithium Extraction: Unlike other battery metals, which are primarily extracted from hard-rock ores using conventional mining techniques, a significant share of the world’s lithium resources is contained in underground reservoirs of highly saline water, known as brines. Brine-based extraction is typically far less capital and energy-intensive, making it a structurally lower-cost than hard-rock mining.

The Investment Angle: These ventures often require significant capital for scale-up. Investors should look for strong partnerships with industrial players. In some fields, like lithium, where production has skyrocketed, there is still substantial room to optimize processes, something that wasn’t a major concern twenty years ago.

Conclusion

The energy transition is about way more than just wind farms and EV. It’s also about how we source the metals that make them possible. Recycling, alternative materials, and smarter refining aren’t just buzzwords, they’re the backbone of a sustainable industrial revolution.

The good news? This field is buzzing with startups, innovations, and new ideas. The bad news? Scaling them fast enough is tough. But one thing’s for sure: the way we treat metals today will decide how green our future really is.

Because in the end, the clean energy revolution isn’t just about switching fuels, it’s about changing the very foundation of our industrial system.

Thanks for reading this article. Please feel free to reach out if you’re working on a solution that we’ve missed, we’d love to chat!