Energy & AI

AI is reshaping every layer of the energy system. This deep dive outlines the structural shifts underway, the data bottlenecks limiting adoption, and the three verticals where we believe AI can create the strongest impact.

1. Structural Shifts in the Energy System

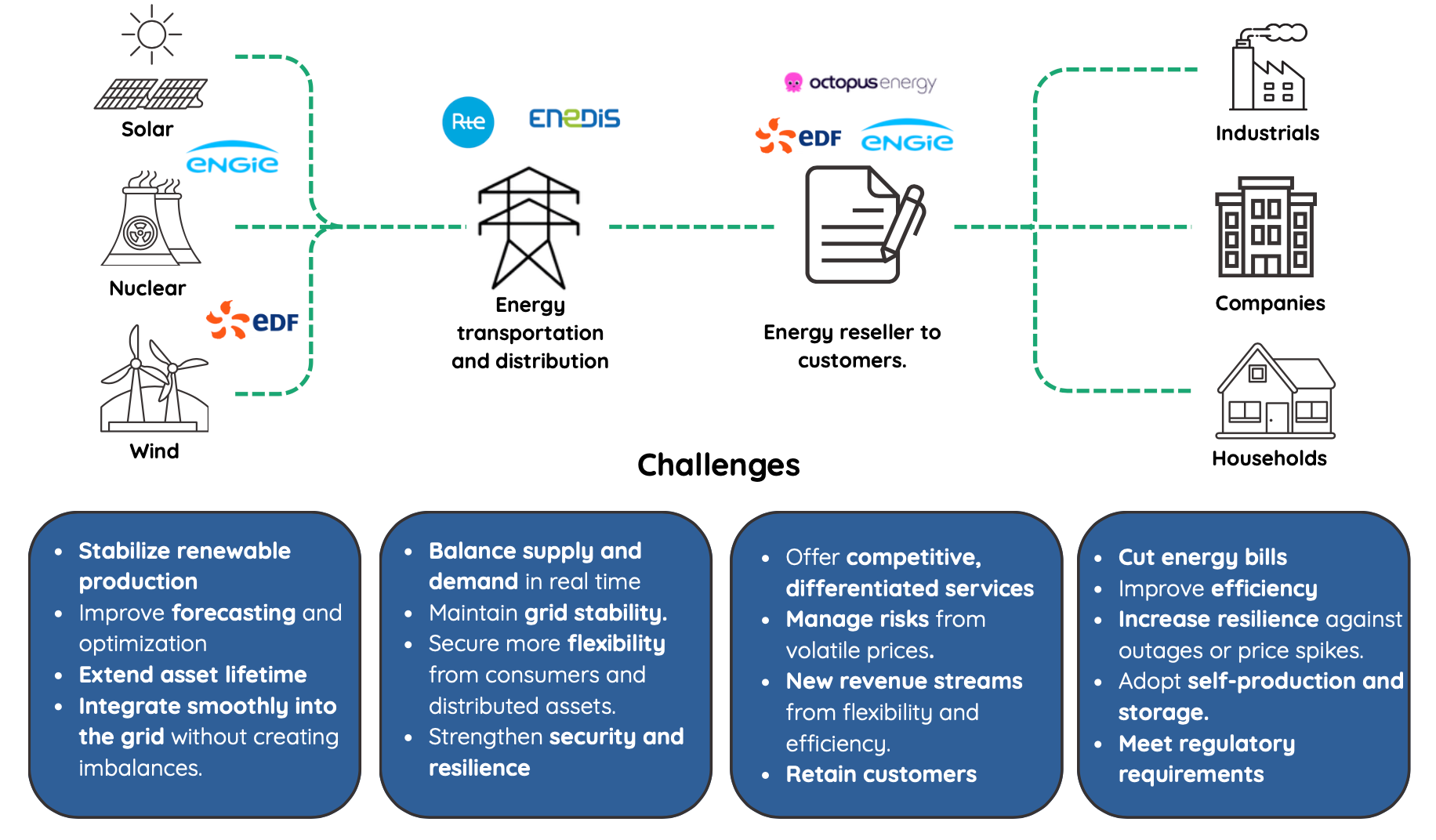

The energy sector is at a critical juncture, facing the dual challenge of rising demand and growing instability.

Global electricity consumption is expected to double by 2050 (IEA, Net Zero by 2050), driven by the electrification of transport, heating, and industry. At the same time, renewables are set to double their share in the power mix by 2040 (Ember, 2025), making power generation more variable over time and turning price volatility into a core parameter of the market.

This volatility translates into a structural need for flexibility. ENTSO-E projects that Europe will require three times more flexibility capacity by 2030 to maintain system balance. On top of this, new sources of demand are emerging: EVs could represent nearly 10% of global demand by 2030 (IEA, 2024), while data centers are on track to double their electricity use by the end of the decade (IEA, 2024).

“We now need to match more flexible consumption (EVs, heat pumps) with production that is increasingly weather-sensitive.” (Vincent Maillard, Octopus Energy France - La SunTech event on energy flexibility, Sept. 25, 2025)

This imbalance between rising demand, variable supply, and the urgent need for flexibility is reshaping the energy value chain, forcing every stakeholder - from generation to consumption - to adapt.

2. AI: The New Control Layer for Energy

AI brings real value in addressing these challenges. With AI model capabilities improving 15–30% each year, the technology has now reached industrial maturity. It can process fragmented datasets to forecast renewable output, balance distributed assets, enable demand response, and improve maintenance unlocking concrete opportunities across the entire energy system, from generation to end-users.

The following breakdown highlights how these opportunities unfold across the value chain.

Yet all these opportunities share the same bottleneck: data. According to KPMG (2025), poor data quality is the leading obstacle to AI adoption in energy (quoted by 24% of organizations) making reliable, integrated, real-time information the critical enabler to turn AI from promise to practice.

3. Bridging the Data Gap

Energy data is massive, fragmented, and inconsistent. On the production side, solar farms, batteries, and wind turbines generate real-time outputs as well as forecasts that depend on weather conditions. On the demand side, smart meters, HVAC systems, industrial machines, and EVs continuously generate load data. Networks add SCADA signals on voltage, frequency, and grid congestion, while external inputs such as market prices and balancing needs must also be integrated.

“At the level of a VPP, we aggregate over 10 million data points per day.” (Julian de Jonquières, CEO of Marmot Energy).

The challenge is not only data volume but also time scale mismatch. Some data refresh every 20–60 milliseconds (synchrophasors/PMUs), SCADA points every 1–2 seconds, smart meters every 15 minutes, and market signals in 5–15 minute intervals. It’s like trying to conduct an orchestra where each musician plays in a different time zone.

On top of that, data fragmentation and quality problems are significant: formats range from CSV and JSON to OPC-UA and Modbus, while data is often noisy, missing, or inconsistent - for example, smart meter datasets frequently show 10–20% of values that are missing or unreliable (SERL Smart Meter Data Quality Report, 2024).

Assets can also be geographically dispersed, adding challenges related to latency (ensuring time-critical data arrives within control deadlines), orchestration (synchronizing heterogeneous assets operating on different protocols and time scales), and cybersecurity (securing a widely distributed, multi-vendor attack surface).

In short, the main challenge is being able to bring together and coordinate billions of fragmented, multi-frequency data points into a reliable, unified control layer. This bottleneck affects the entire energy stack, and solving it is the prerequisite for any AI solution to scale. Given these dynamics, we see a few verticals where the need is most acute and the opportunity to build category-defining companies is the strongest.

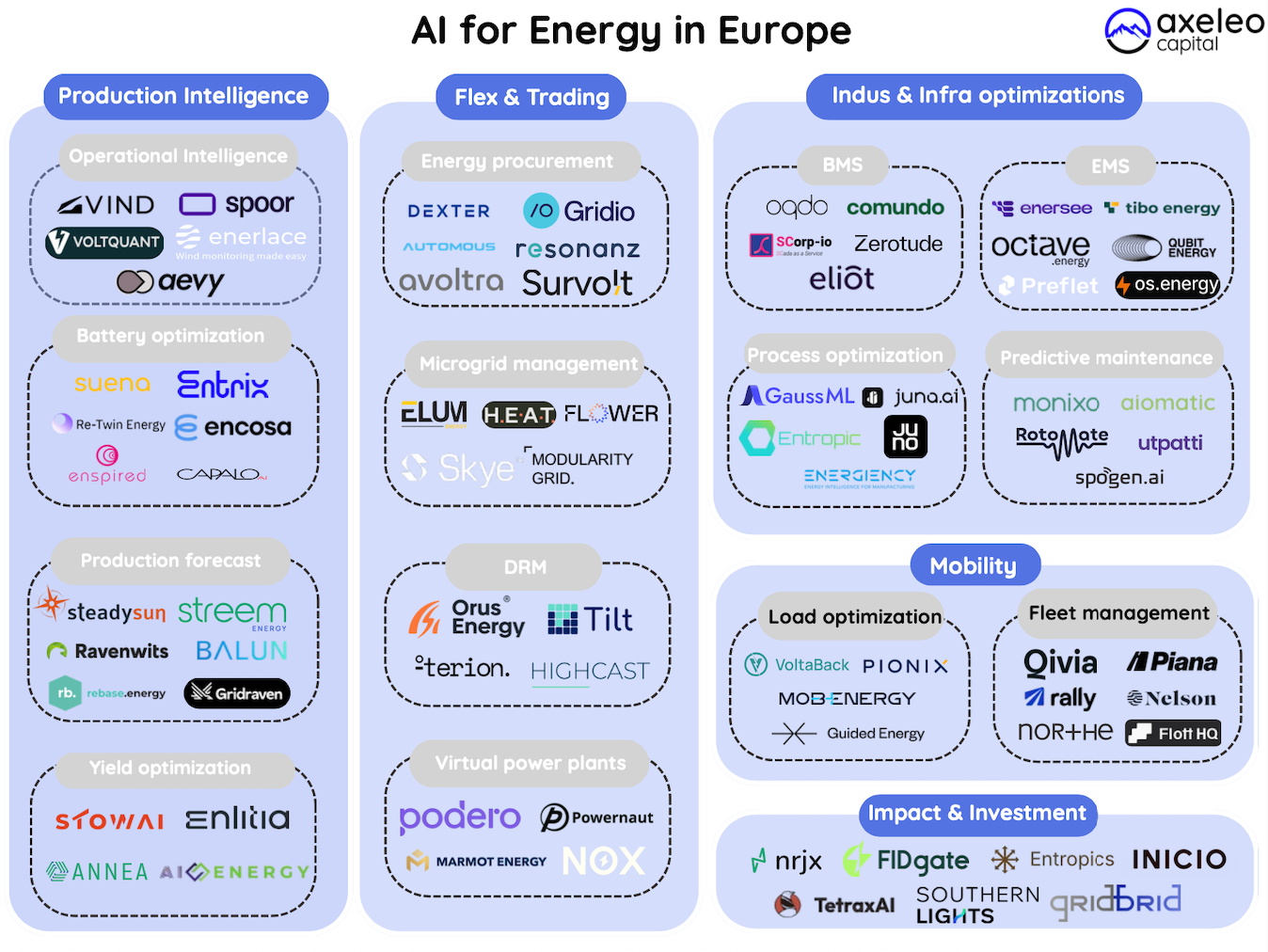

4. Our takes on AI applied to Energy

Based on our analysis, three verticals stand out as the strongest opportunities for AI in energy.

- VPPs & DRM: Turning Volatility into ValueAs renewables are expected to exceed 60% of the energy mix by 2030, the grid’s biggest structural challenge will be balancing supply and demand in real time. The mismatch between production peaks and consumption needs is already driving price volatility and stressing networks. With Europe’s flexibility requirements set to triple by 2030 (ENTSO-E), we see this not as a constraint but as one of the most attractive opportunities in the energy sector: solutions that can unlock, aggregate, and monetize flexibility.

Our conviction is that the next generation of winners will be those who manage to capture distributed flexibility at scale. Virtual Power Plants (VPPs) are one path, pooling thousands of resources and orchestrating them as if they were a single power plant. Demand Response Management (DRM) complements this by shifting or reducing consumption during peaks, stabilizing the grid while lowering costs. The market is already sizable, with European demand response revenues above €3B in 2023 and growing >15% annually.

In this space, Tilt Energy illustrates how a new generation of players is positioning itself as a flexibility valorizer. While traditional aggregators tend to focus on large industrial players (e.g., Voltalis, EnelX, Centrica), Tilt addresses the long tail of SMEs and commercial buildings, an often-overlooked segment that represents a vast reservoir of untapped flexibility. By connecting site-level assets such as HVAC, refrigeration, or EV charging, Tilt aggregates businesses into demand response programs and helps them monetize their flexibility. The value proposition is clear: companies cut their energy bills by 10–30% while creating new revenue streams, and Tilt captures part of that upside. With AI-driven orchestration increasing the amount of revenue-generating flexibility, we believe this segment has the potential to create category-defining players.

- Microgrid Controllers: The OS for C&I Energy

Global electricity demand is projected to grow by 3.3% in 2025, more than twice the pace of overall energy demand. This acceleration is straining grids already challenged by volatility and has pushed corporates to deploy on-site renewables and storage. Yet most of these assets remain siloed and poorly coordinated, limiting both efficiency and economic return.

Microgrid controllers are emerging as a critical layer of enterprise energy infrastructures. By integrating and orchestrating solar panels, batteries, EV chargers, heat pumps, and generators, they give C&I sites the ability to manage their energy flows as an asset rather than a cost. The value proposition goes beyond resilience: controllers decide when to consume, store, or sell electricity back to the grid, directly impacting OPEX and improving the ROI of on-site generation and storage investments. In our view, this category is set to become indispensable as corporates look to hedge against volatility and actively manage their energy portfolios.

One company illustrating this approach is HEAT Solutions, which has built a universal, plug-and-play software layer for C&I energy systems. The platform connects all major assets through a single interface and orchestrates them in real time based on market signals. Backed by AI, it improves forecasting accuracy by up to 30% (Fraunhofer ISE, 2022) and reduces energy costs by 10–15% (McKinsey Energy Insights, 2022), making energy systems more autonomous and significantly improving the ROI of on-site generation and storage.

- EMS 2.0: The Control Tower for Energy Managers

Buildings account for over 40% of Europe’s final energy use (Eurostat). With energy prices still 30–50% above pre-2021 levels (IEA) and regulation requiring annual reductions in consumption, corporates face mounting pressure to cut OPEX while staying compliant. Yet energy managers are stuck with fragmented systems between sites, scattered data across buildings, and little ability to coordinate at portfolio scale.

Next-generation Energy Management Systems (EMS 2.0) aim to solve this by sitting on top of existing infrastructure and centralizing data from all sites. Acting as a one-stop shop for all energy data and operations, and as a single source of truth across sites, they give energy managers a unified interface to turn raw data into actionable insights, driving both efficiency gains and compliance.

A relevant illustration in this category is Enersee, which positions itself as an AI-powered intelligence layer built on top of existing EMS platforms. By aggregating and analyzing energy data, it reveals inefficiencies that usually stay under the radar. The upside is significant: AI-powered EMS can cut site-level consumption by up to 30%, translating into 15–25% OPEX savings.

It is undeniable that AI will be central to unlocking flexibility. The real question is who will succeed in penetrating the market with a solution capable of aggregating and orchestrating the massive, fragmented data required to make it work.

At Axeleo Capital, we’re actively exploring this space — if you’re building here, we’d be glad to connect !